Efforts to Address Climate Change(Disclosure Based on TCFD Recommendations)

In January 2020, SPARX Group (together with its group companies, the "Group") announced its agreement with the recommendations published by the Task Force on Climate-Related Financial Disclosures (TCFD) as part of its active involvement in realizing, through investment, a society in which human beings can coexist with the global environment.

The following is a report on the status of our efforts to meet the TCFD recommendations for FY2024, which ended on March 31, 2025 per its recommended disclosure categories of Governance, Strategy, Risk Management, and Metrics and Targets linked to climate change-related risks and opportunities.

Governance

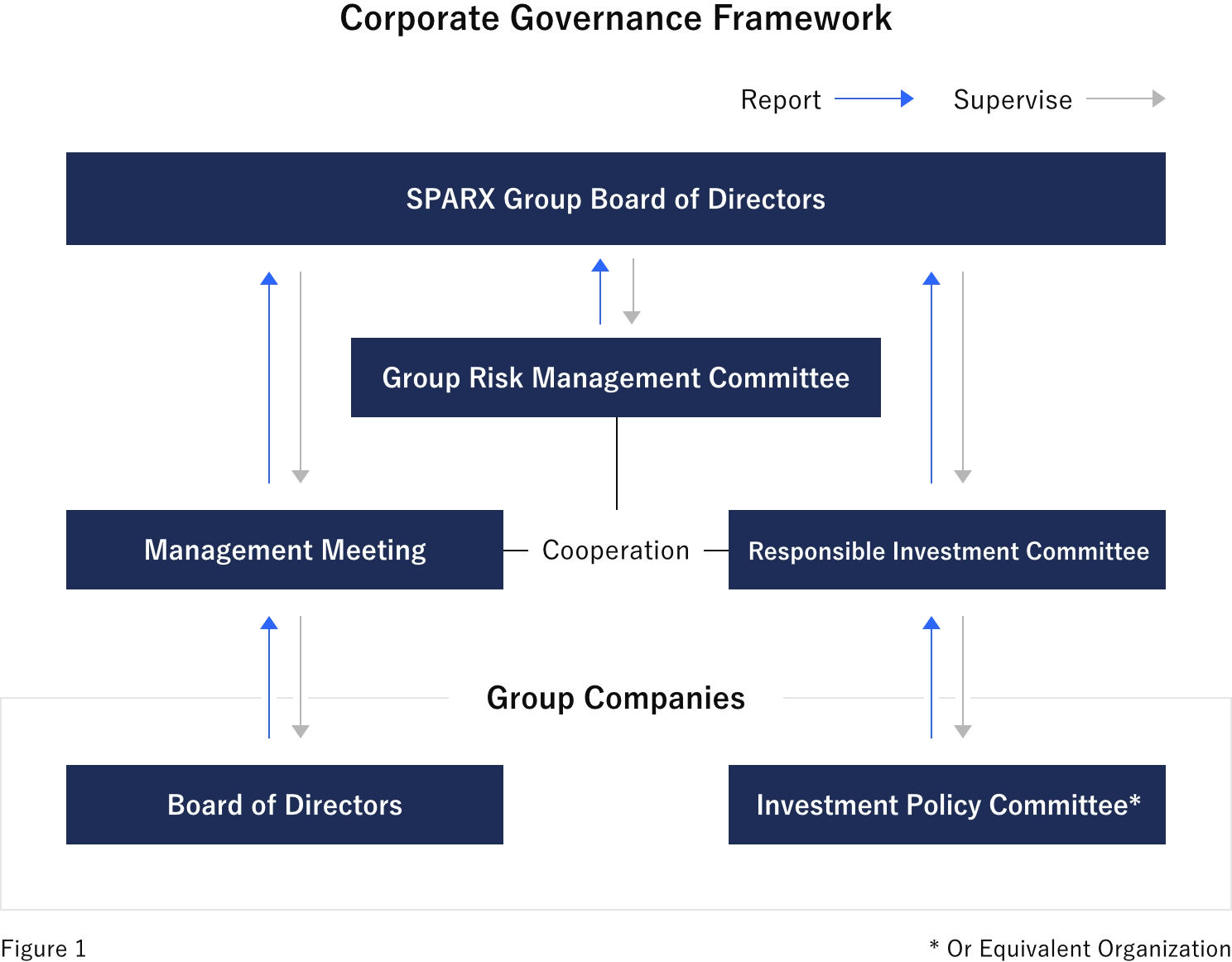

The Group has formulated a Basic Sustainability Policy based on its recognition that addressing climate change and other sustainability-related issues is one of the most crucial aspects of management. Thus, we have built a governance structure based on the Board of Directors Meeting and the SPARX Group Management Meeting. The Board of Directors debates and decides on the climate change issues related to this basic policy and supervises the Management Meeting, the central decision-making body for day-to-day corporate operations. The Management Meeting discusses and decides on specific sustainability policies and promotion strategies at least annually and when otherwise necessary and reports its activities to the Board.

The Board of Directors, consisting mostly of outside directors, also verifies and discusses the progress of these specific policies and promotion strategies to ensure appropriate management and continuous improvement through the PDCA cycle. The Management Meeting, which includes all full-time Directors and Group Executive Officers at the core of corporate operations, meets at least once a month and promptly reports its activities to the Board of Directors. We have also established a Sustainability Planning department to facilitate specific discussions on sustainability management at the Management Meeting.

Strategy

The Group recognizes that maintaining a sustainable global ecosystem and environment is essential for the medium- to long-term management of client assets. In particular, the Group sees climate change issues as vital in achieving this objective.

Climate change presents associated risks and opportunities due to the severe natural disasters caused by rising average temperatures and the socioeconomic changes brought about by the shift to a carbon-free society.

There are two types of risks: physical risks can be acute--caused by increases in natural disasters and extreme weather events--or chronic--stemming from rising average temperatures; and transition risks result from stricter regulations meant to eliminate society's carbon dependence and responses to adopting decarbonization technology.

Opportunities include potential corporate revenue from technological innovations and market changes addressing climate change problems. The Group supports and promotes solutions addressing climate change and the transition to a carbon-free society by providing new investment products, leading to more business opportunities and helping achieve a sustainable environment and society.

Based on the TCFD's recommendations, the Group is working, as shown below, to understand the opportunities, physical risks, and transition risks from short-, medium-, and long-term perspectives. The direct impact of climate change on the Group as an investment company should be less significant than in other industries. However, we will examine these assumptions by analyzing multiple scenarios to understand more specific financial and other effects. To prepare for physical risks from large-scale natural disasters, the Group regularly reviews its BCP and bolsters its management systems to maintain business continuity.

Climate-Related Risks

- [Expected periods] Short term: 0-3 years, medium term: 3-10 years, long term: 10-30 years

Opportunities from Climate Change

When considering measures to address the above climate-related risks, we can redefine them as business opportunities and tie them to ideas for investment strategies. For instance, the risk of a "delayed response to changes in industrial structure due to rapid technological innovation" would become "finding investment opportunities in companies that possess technologies that will bring about rapid changes in the industrial structure and incorporating them into investment strategies."

Risk Management

The Group has instituted its Basic Group Risk Management Rules to establish an essential risk management framework, identifying in advance expected individual risks and managing them appropriately. As a result, we address the Group's risks and ensure its soundness and integrity.

Moreover, the SPARX Group Board of Directors has established a Group Risk Management Committee to review and deliberate on corporate and Group risk management matters. The Group Risk Management Committee includes all full-time Directors and Group Executive Officers at the core of corporate operations and meets once a quarter as a general rule. The Group Risk Management Committee follows the risk management process stipulated in the Basic Group Risk Management Rules to identify potential expected risks and emergent material phenomena, recognize and assess risks, develop and implement countermeasures, and monitor how these countermeasures work.

The Group Risk Management Committee also reports its minutes to the Board of Directors in a timely manner. The Board of Directors, consisting mostly of outside directors, monitors risk locations, types, countermeasures, and their implementation and supervises the risk management process. In this role, the Board establishes and continually improves an appropriate risk management approach for the Group's management circumstances and strategies.

Currently, the Group manages climate-related risks not as a risk category set and governed under the Basic Group Risk Management Rules but as a factor with a potential general impact on all risk categories. We will continue improving and strengthening our risk management approach to climate change issues.

Metrics and Targets

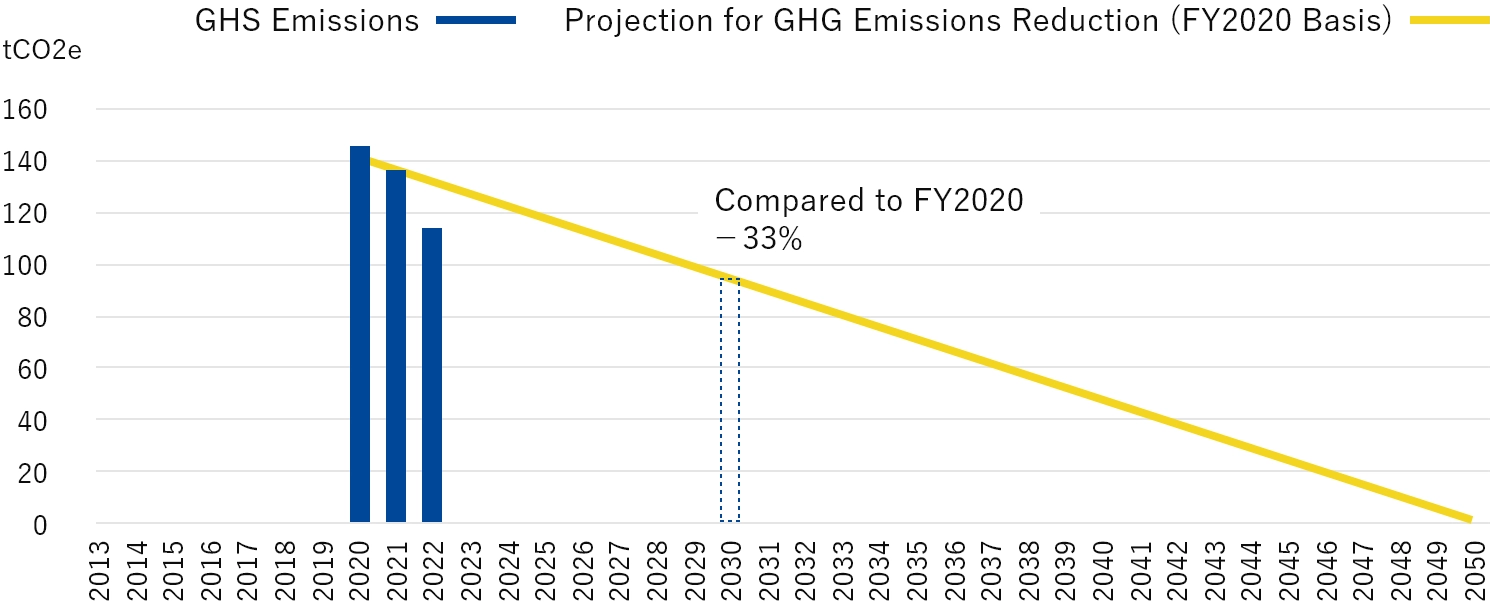

The Group aims to achieve carbon neutrality by 2050 and promotes initiatives toward realizing a carbon-free society. We have set greenhouse gas ("GHG") emissions as a key indicator in our goal to mitigate climate-related risks and realize opportunities. We have established specific reduction targets as we continuously monitor our progress. All Group companies report their progress in these metrics to the Management Meeting and the Board of Directors annually or as otherwise required.

The GHG emissions generated by the Group's business activities in FY2024 (the total of Scope 1 and Scope 2*1) were approximately 86.67 tCO2e, a 39.0% decrease from FY2020. In September 2022, as part of our efforts to reduce GHG emissions, we switched to electricity derived from renewable energy sources with non-fossil certificates for buildings occupied by all our domestic Group companies. This initiative successfully reduced our emissions. However, emissions increased last year due to the greater office space required for our business growth. We have achieved our interim target of a 33% reduction in GHG emissions by FY2030 (compared to FY2020), but we will continue working toward further reductions.

In addition to monitoring progress on our Scope 1 and Scope 2 reduction targets, we continue to calculate and monitor the CO2 emissions of our entire supply chain (Scope 3) using the Ministry of the Environment's Green Value Chain Platform and other tools. We also recognize that our calculation in Category 15: Investments and Loans, which aims to enhance our Scope 3 disclosure, is a crucial first step for a financial institution in helping to realize a carbon-free society. We are preparing data to measure GHG emissions (Financed Emissions) through investments and loans based on the PCAF*2 method.

Scope1・2 tCO2e

| FY2020 | FY2022 | FY2023 | FY2024 | |

|---|---|---|---|---|

| Scope1 (direct emission) | 6.05 | 6.13 | 5.30 | 4.13 |

| Scope2 (indirect emission)*3 | 135.93 | 103.67 | 75.66 | 82.54 |

| Scope1・Scope2 Total | 141.98 | 109.80 | 80.96 | 86.67 |

| Reduction Results (Compared to FY2020) | - | 22.7% | 43.0% | 39.0% |

| Reduction Results (Compared to previous year) | - | 17.3% | 26.3% | 7.1% |

Scope3 tCO2e

| Category | FY2022 | FY2023 | FY2024 | |

|---|---|---|---|---|

| Scope3 | Category1 (Purchased Goods and Services) |

2.81 | 4.23 | 3.98 |

| Scope3 | Category2 (Capital Goods) | 249.23 | 124.47 | 1,467.81 |

| Scope3 | Category5 (Waste Generated in Operations) |

0.39 | 0.36 | 0.54 |

| Scope3 | Category6 (Business Travel) | 576.47 | 822.59 | 1,115.39 |

| Scope3 | Category7 (Employee Commuting) | 51.70 | 54.36 | 56.35 |

[Calculation period]

Each period : From April 1 to March 31 in the following year

[Calculation scope]

Scope 1 & Scope 2: All domestic Group companies*4 (excluding SPARX Tomakomai Green Hydrogen Production Plant*5), SPARX Asset Management Korea Co., Ltd. *6, SPARX Asia Investment Advisors Limited*6

Scope 3:All domestic Group companies*4 (excluding SPARX Tomakomai Green Hydrogen Production Plant for Categories 1, 5, and 6*5)

[Calculation methods]

Our Scope 3 calculation method and emission figures are based on the "Basic Guidelines on Accounting for Greenhouse Gas Emissions Throughout the Supply Chain Ver. 2.7" and "Emission Unit Value Database for Accounting of Greenhouse Gas Emissions by Organizations Throughout the Supply Chain Ver 3.5" from the Ministry of the Environment and the Ministry of Economy, Trade and Industry.

Category 1: Calculated by multiplying the cost of copy paper purchased by all the domestic Group companies*4 by the emission unit values

Category 2: Calculated by multiplying the value of fixed assets acquired by all the domestic Group companies*4 in the relevant fiscal year by the emission unit values

Category 5: Calculated by multiplying the waste generated by all the domestic Group companies*4 by the emission unit values by waste type and disposal method

Category 6: Calculated based on the amount of domestic and international business travel by all the domestic Group companies*4 (multiplied the cost for using airlines, rail, buses, and taxis by the emission unit values)

Category 7: Calculated from the yearly total of the monthly commuting expenses of employees of all the domestic Group companies*6 at the end of the relevant fiscal year (multiplied the cost of using rail and buses by the emission unit values)

- *1 GHG emissions calculation criteria are Scope 1 (direct emissions) + Scope 2 (indirect emissions) based on the GHG Protocol.

- *2 Partnership for Carbon Accounting Financials

- *3 Scope 2 is calculated based on the market-based method.

- *4 In FY2024, all the domestic Group companies were as follows:

SPARX Group Co., Ltd.

SPARX Asset Management Co., Ltd.

SPARX Green Energy & Technology Co., Ltd.

SPARX Asset Trust & Management Co., Ltd.

SPARX Investment Co., Ltd.

Up to FY2023, all the domestic Group companies were as follows:

SPARX Group Co., Ltd.

SPARX Asset Management Co., Ltd.

SPARX Green Energy & Technology Co., Ltd.

SPARX Asset Trust & Management Co., Ltd.

SPARX Investment Co., Ltd.

SPARX Innovation for Future Co., Ltd.

In April 2025, SPARX AI & Technologies Investment Co., Ltd. changed its name to SPARX Investment Co., Ltd. In April 2024, SPARX Innovation for Future Co., Ltd. was dissolved. - *5 We excluded items with little impact during FY2024 from the calculations for the SPARX Tomakomai Green Hydrogen Production Plant, which started operation in March 2025.

- *6 We use the emissions coefficients for each country where the offices are located.

Reduction of CO2 Emissions from SPARX's Business Activities

Disclosure Based on TCFD Recommendations on Responsible Investment

The following describes the portfolio management efforts of asset management companies within the Group to analyze and assess the impact of their portfolio companies' response to climate change.

Governance

The Group upholds its purpose "to make the world wealthier, healthier, and happier (through investment)." We identify and manage apparent and latent risks and opportunities related to all client assets to realize this purpose. Furthermore, we have established a separate Responsible Investment Committee, chaired by the Group CIO, as an advisory body to the Board of Directors of SPARX Group in order to fulfill our responsibility for oversight and accountability for responsible investment.

The Responsible Investment Committee, which includes all full-time Directors and Group Executive Officers, meets at least once a quarter and promptly reports its findings to the Board of Directors. In addition, we have established the Responsible Investment Promotion department to promote concrete discussions on the implementation of PRI (Principles for Responsible Investment) in the Responsible Investment Committee.

The Committee hears reports from the Group companies' investment policy committees (or equivalent organizations) on their responsible investment practices, including how they address climate-related risks and opportunities and respect of human rights. It also endorses annual reports on responsible investing and approves changes to provisions on handling climate-related risks and opportunities and respecting human rights in the Responsible Investment Policy and other policies.

Responsible Investment Committee meetings are attended by external advisors who provide independent advice on the reports and deliberations while sharing their thoughts on the latest trends in responsible investing.

In FY2024, the Responsible Investment Committee met four times, during which it heard reports on responsible investment practices from all Group investment policy committees, reviewed the Responsible Investment Policy, and approved the annual report.

- Please refer to figure 1 for Corporate Governance Framework

Strategy

To resolve climate change, we must encourage portfolio companies to incorporate and address climate change-related risks and opportunities in their medium- to long-term business strategies. As an asset manager, we have asked S&P Global to conduct scenario analysis of the portfolios of the Listed Equity Investment strategy as well as listed alternative equities investment strategy , which account for most of our assets under management as of December 31, 2024. The analysis aims to uncover the impact of climate change-related risks and opportunities on our clients' asset portfolios.

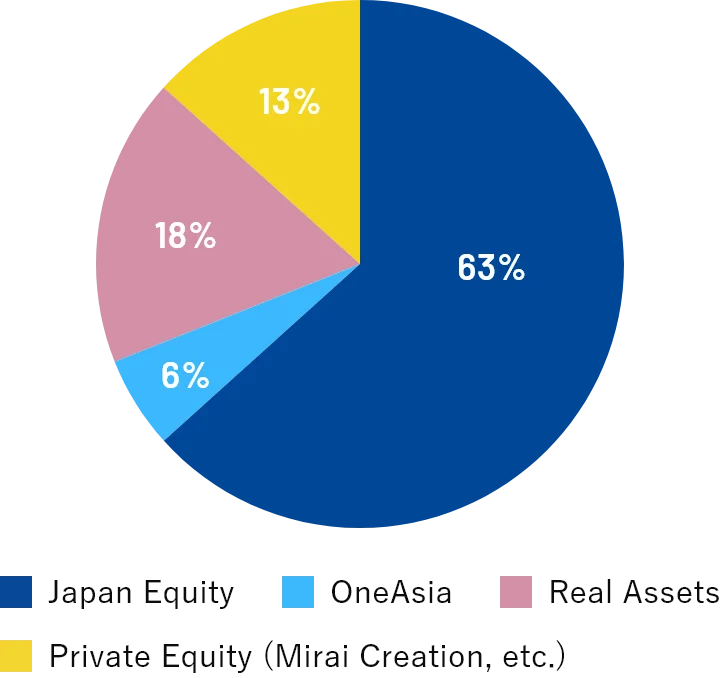

The Group's AUM by Investment Strategy as of December 31, 2024 are as follows:

| Japanese Equity | 13,772 |

|---|---|

| OneAsia | 1,033 |

| Real Assets | 2,812 |

| Private Equity*2 (Mirai Creation, etc.) |

1,739 |

| Total | 19,357 |

- *1 The Listed Equity and Listed Alternative Equity Investment Strategies" are the sum of "Japanese Equity" and "OneAsia" shown above.

- *2 Our Private Equity Investment Strategy (Mirai Creation Funds) represents JPY132B of the Private Equity shown in the table.

Compliance with well below 2°C target: Evaluating transitions away from greenhouse gases

We evaluated the portfolios and benchmarks of our Listed Equity and Alternative Equity Investment Strategies*3 for their compliance with international targets for combating global warming based on a transitionary approach. We used S&P Global's assessment on pathways to net-zero emissions to determine how well our portfolios aligned with the Paris Agreement target of well below 2°C.

In this evaluation, we look at past performance and future (medium-term) forecasted emissions to verify whether our portfolio companies' emission reductions over time are at an appropriate level in line with the global warming prevention targets. We concluded that the portfolios of our Listed Equity and Alternative Equity Investment Strategies once again fell between 2°C and 3°C, while their benchmarks were assessed to be in the range of above 1.5°C and below 2°C*4. Going forward, we will internally examine how we can align our portfolios to a level well below 2°C.

- *3 The Listed Equity and Alternative Equity Investment Strategy benchmarks are a composite of TOPIX, KOSPI, and MSCI Asia ex Japan indices, weighted by the assets under management in the corresponding markets.

- *4 There was no significant change in data coverage in the comparison between the results of last year's and this year's analyses of alignment with the target of under 2°C (see below for details). However, the companies within the benchmark that have relatively large market capitalization had made progress in their data disclosure, so the analyses used fewer estimates from S&P Global and more disclosed data from the companies themselves. This shift is likely one of the primary factors for improved alignment with the benchmark's target of under 2°C.

| Coverage | 2023 | 2024 | ||

|---|---|---|---|---|

| Portfolio | Benchmark | Portfolio | Benchmark | |

| Carbon Performance | 100% | 100% | 100% | 100% |

| Paris Agreement Compliance | 95% | 99% | 96% | 99% |

| Scenario Analysis - Carbon Pricing | 96% | 99% | 100% | 100% |

| Scenario Analysis - Physical Risk | 100% | 100% | 100% | 100% |

Transition Risks

The TCFD classifies climate-related risks into two categories: transition risks and physical risks. Transition risks are related to the move toward a carbon-free economy, while physical risks are associated with the physical impact of climate change.

We assessed the financial impact of climate-related risks (e.g., the economic impact of future carbon prices) on our Listed Equity and Alternative Equity Investment Strategy portfolios.

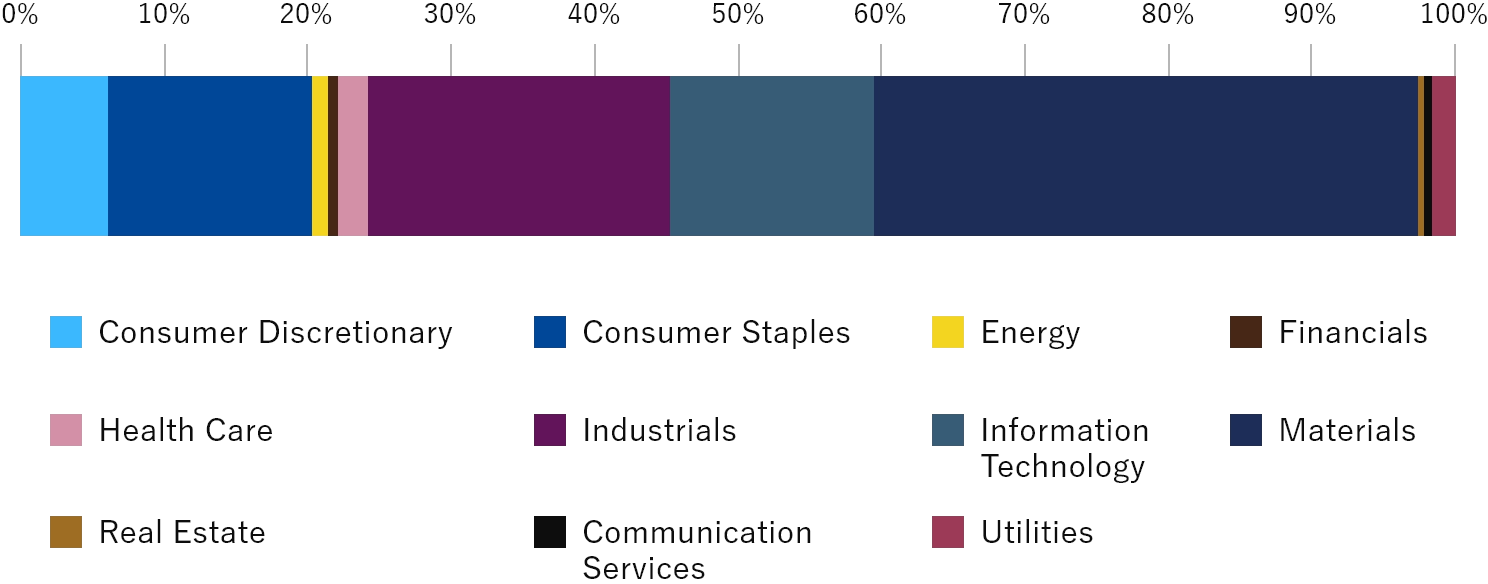

The estimated future unpriced cost of carbon (UCC) borne by the portfolios of the Listed Equity and Listed Alternative Equity Investment Strategies is higher in Japan, by region, and in materials, capital goods, and services, by sector. Therefore, these strategies' portfolios will likely see the most significant impact from the risk of climate-related policy changes that result in higher carbon costs in Japan. The EBITDA-at-risk, representing the current ability of portfolio companies to cover their future carbon costs, was approximately 6.56% on a portfolio-weighted average basis in 2030, based on the high-risk scenario*5, while the benchmark was about 11.07%. Focusing on the percentage of portfolio companies at risk of a 10% or greater decline in EBITDA, we observed more progress in 2024, with 10.68% for the portfolios and 12.64% for the benchmark, compared to 16.48% and 16.87%, respectively, in 2023.

- *5 The scenario with the temperature rise limited to well below 2°C by 2100 is consistent with the Paris Agreement and is based on OECD and IEA studies.

| 2023 | 2024 | |||

|---|---|---|---|---|

| Portfolio | Benchmark | Portfolio | Benchmark | |

| EBITDA at Risk | 6.80% | 11.44% | 6.56% | 11.07% |

| Weight > 10% at Risk | 16.48% | 16.87% | 10.68% | 12.64% |

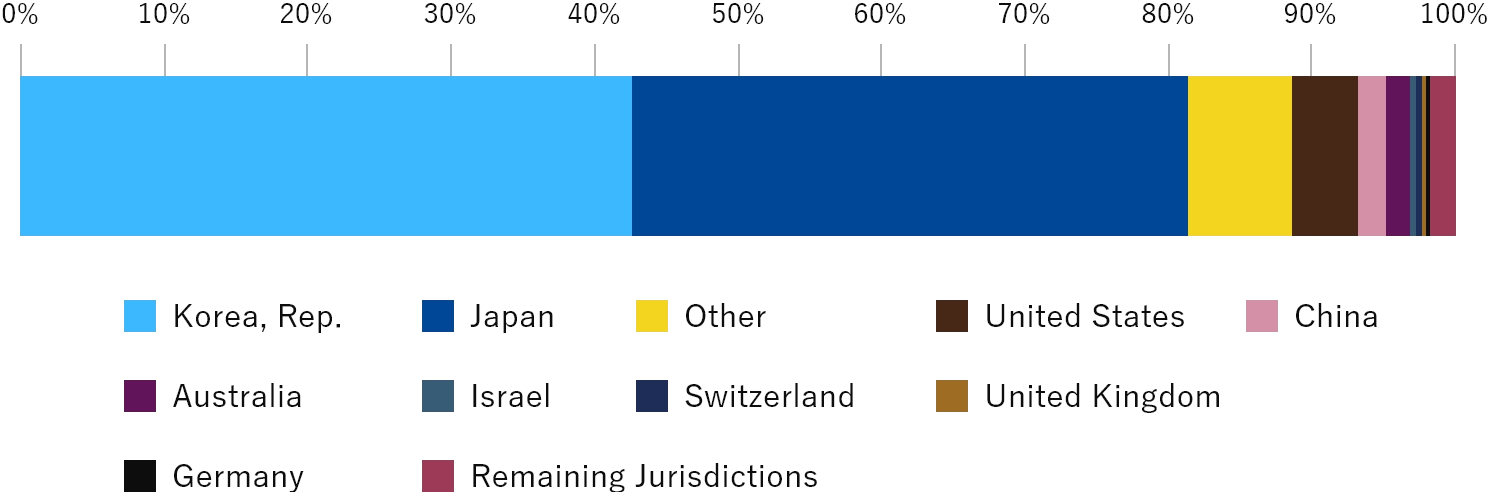

Breakdown of UCC by Sector

Breakdown of UCC by Country

Physical Risks

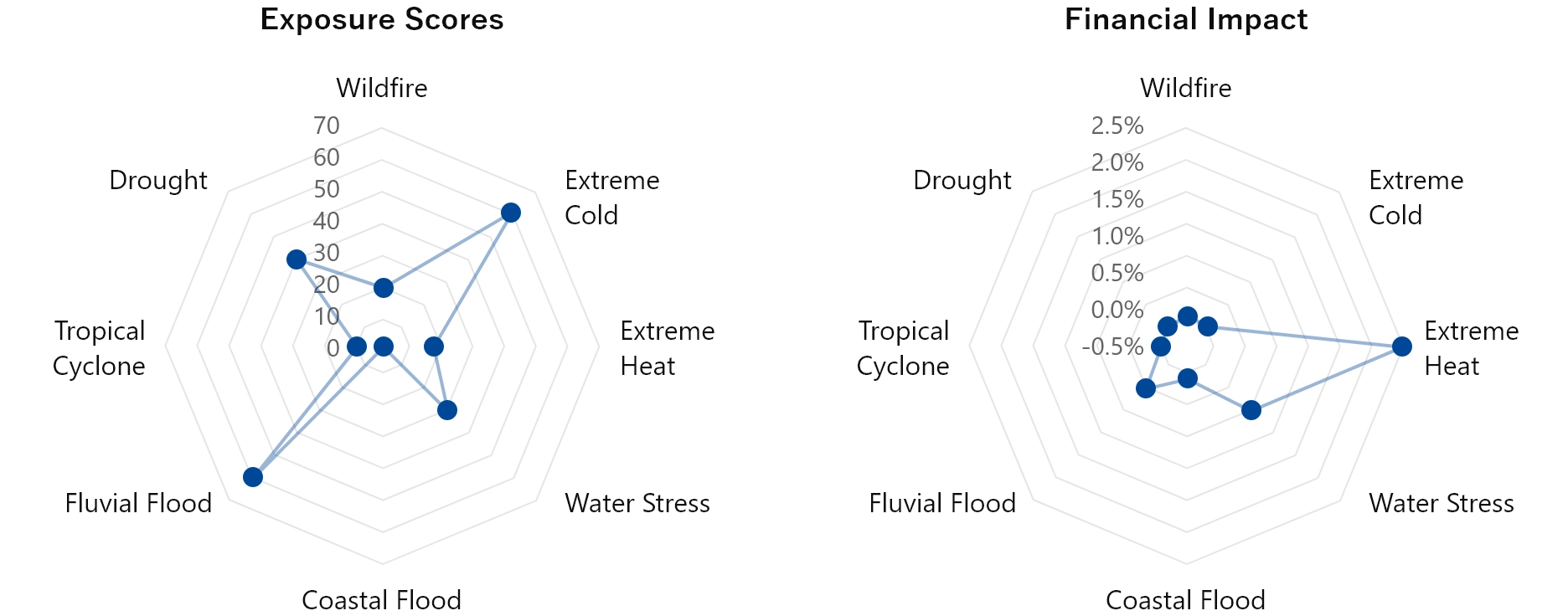

We assessed the physical risks for our Listed Equity and Alternative Equity Investment Strategy portfolios based on moderate-to-high-risk scenarios for 2050*6. Of the nine hazard types (wildfires, cold waves, heat waves, water stress, coastal floods, fluvial floods, urban floods, tropical cyclones, and droughts), heat waves had the highest exposure scores. Heat waves also had the highest financial impact.

Source: Prepared by SPARX based on the S&P Global data

- *6 The scenario with a temperature increase of 2.8-4.6°C by 2100 corresponds to a Shared Socioeconomic Pathway (SSP) score of 3 and a Representative Concentration Pathway (RCP) score of 7.0. Exposure scores are expressed on a scale of 1 to 100, where 100 represents the maximum possible risk, and 1 is the minimum possible risk. The financial impact is expressed as a percentage (%) of the asset value of possible losses (e.g., capital expenditures, operating expenses, business interruption) that may occur due to climate change.

Risk Management

In researching and analyzing portfolio companies and making investment decisions, the Group emphasizes the qualitative evaluation of companies through bottom-up research. "Bottom-up research" refers to our qualitative evaluation of ESG-related opportunities and risks, alongside our estimates of expected investment returns.

Moreover, the Group is working to develop a framework that enables it to encourage portfolio companies to promote climate change-related initiatives, while utilizing climate change-related data from external vendors in selecting and engaging with partners.

We reference climate change-related data from external vendors for the Listed Equity and Alternative Equity Investment Strategy portfolios. For each portfolio and benchmark (or reference index), we measure the carbon footprint (the CO2 equivalent of greenhouse gas emissions resulting from business activities) and weighted average carbon intensity (WACI).

We then report these figures to the Investment Policy Committee and our engagement numbers to the Responsible Investment Committee every quarter.*7

- *7 We began reporting our engagement numbers to the Responsible Investment Committee in January 2023.

Metrics and Targets

As an investment company and a corporation, the Group supports the long-term goals of the Paris Agreement and is committed to taking proactive steps to limit the rise in average global temperatures. As an investment company, the Group will continue to support all our portfolio companies and investments in setting a goal of achieving net-zero GHG emissions by 2050 by advancing related initiatives.

Below are our calculations for the TCFD's recommended disclosure requirements of carbon footprint (the equivalent CO2 resulting from business activities) and weighted average carbon intensity (WACI) for our Listed Equity and Alternative Equity Investment Strategy portfolios as of December 31, 2024.

| 2023 | 2024 | |

|---|---|---|

| Carbon Footprint | 451,291 tCO2e | 349,189 tCO2e |

| WACI | 78 tCO2e/million USD | 57.57 tCO2e/million USD |

For both the carbon footprint and WACI calculations above, we utilized S&P Global's data to calculate GHG emissions based on portfolio company disclosures or a proprietary approach using modeling when information was not available. We calculate Scope 1 and Scope 2 emissions with this approach. Our policy for the Group's assets under management is to actively utilize GHG emission ratings and external evaluation organization assessments to supplement our analytics. However, due to differences in data reliability and evaluation methods, we do not compare figures directly; instead, we prefer to monitor data continuously and consider its future use options.

Targets by individual strategy among managed client assets

(The Listed Equity and Listed Alternative Equities Investment Strategies)

The Listed Equity and Listed Alternative Equities Investment Strategies

These investment strategies reflect our support for the long-term goals of the Paris Agreement and our commitment to taking proactive steps to limit the rise in average global temperatures. Therefore, we will help all our portfolio companies set the goal of achieving net-zero GHG emissions by 2050 and advance related initiatives toward this goal.

To achieve this goal, we believe it ideal for our portfolio companies to formulate and implement greenhouse gas reduction plans that comply with the Paris Agreement.

However, as part of this process, we must support companies that are likely to implement future reductions rather than investing only in companies with low emissions or those that have reduced their carbon output under the Paris Agreement.

Thus, we have set an interim target of having at least 40% of the portfolio companies in all funds under the Japanese Equity Investment Strategy declare their commitment to the net-zero goal by 2030 as we help progress corporate efforts toward carbon neutrality*8

- *8 The strategy of investing in Japanese equities within the Listed Equity and Alternative Equity Investment Strategies

Our performance against the target as of December 2024 is as follows:

| Previous target | 2024 performance | |

|---|---|---|

| 2024 | TCFD endorsement rate of 30% or more for all funds in the Japanese Equity Investment Strategy | 97.30% of funds (based on the number of funds) with a TCFD endorsement rate of 30% or higher |

| 2025 | TCFD endorsement rate of 50% or more for all funds in the Japanese Equity Investment Strategy | 94.59% of funds (based on the number of funds) with a TCFD endorsement rate of 50% or higher |

| New target | 2024 performance*9 | |

|---|---|---|

| 2030 | Net-zero declaration rate of 40% or more for all funds in the Japanese Equity Investment Strategy | 62.16% of funds (based on the number of funds) with a net-zero declaration rate of 40% or higher |

- *9 Data for companies that have declared a net-zero target refer to those as of March 31, 2025.

These investment strategies reflect our long-term engagement to support our portfolio companies in formulating and implementing greenhouse gas reduction plans that comply with the Paris Agreement. The following is a leading example of our engagement in 2024.

This investment strategy has engaged with Company A, a mid-sized real estate company that offers a wide range of services. Its operations are based on strict property procurement criteria, underpinning its sound financial position. Since the financial crisis, the company has steadily expanded its business and now has a market capitalization of over JPY 100 billion.

Our engagement centered on the following three points. First, we emphasized the need to present a continuous and clear growth strategy to the stock market that would dispel concerns about a potential downturn in the company's growth rate. Second, with its market capitalization exceeding JPY 100 billion and increased attention from new institutional investors, we requested that the company clearly and concisely disclose information on its diverse business activities. Third, we communicated the importance of clearly disclosing ESG-related policies and initiatives to garner support from a broader range of investors.

Regarding an environmental issue that pertains specifically to the third point, the company's improvement in acquiring green certifications for its mainstay real estate liquidation business should contribute to the long-term enhancement of corporate value. While it is not currently actively pursuing green certification for its buildings, we discussed the possibility that certification would boost the added value of properties, leading to a corresponding increase in rents. The company generally agrees with the significance of green certification. Still, it recognizes that acquiring certification will take some time, given that most of its tenants are small to mid-sized companies with limited rent-bearing capacity. The investment strategy will continue to engage in ongoing dialogue with the company and support its sustainable improvement in corporate value.

Private Equity Investment Strategy (Mirai Creation Funds)

Problems related to the sustainability of the global environment pose a significant risk factor, but they can also present business opportunities for startups. Under this investment strategy, we identify, invest in, and support startups that aim to address environmental issues from various angles. Some may reduce energy consumption by making society more efficient and more intelligent overall. Meanwhile, others utilize hydrogen to reduce greenhouse gas emissions or develop new materials that can help prevent resource depletion.

We will also analyze whether these startups can understand and control their direct and indirect environmental impact and whether their management has a mindset oriented toward environmental conservation.

This investment strategy reflects our support for the long-term goals of the Paris Agreement and our commitment to taking proactive steps to limit the rise in average global temperatures. The Group will continue to support all our portfolio companies and investments in setting the goal of achieving net-zero GHG emissions by 2050 by advancing related initiatives. In the process, our investment managers responsible of this investment strategy will guide our portfolio companies in the financial and non-financial disclosure of their climate change responses.

Our investment strategy managers participate in discussions as guides to assessing climate-related risks and opportunities, as well as their financial implications. These discussions maximize portfolio company commitment to financial disclosure on climate change before these companies go public. Below are examples of when this investment strategy played a guiding role in discussions.

Company B is working to reduce greenhouse gas (GHG) emissions and generate J-Credits through improved management of livestock waste. The dairy industry is expected to face increased scrutiny from environmental groups in the future, so our investment strategy encouraged Company B to be aware of these risks and consider measures to address them before going public. In addition to the management team, we also consulted with outside directors to raise awareness of the risks and opportunities. We will continue to propose measures to address environmental issues, including the provision of clear and transparent disclosure with CO₂ emission visualizations.

Company C develops and manufactures chemicals used for gas adsorption and catalytic applications. Its strength lies in its ability to produce these chemicals at low cost while reducing its environmental impact. The investment strategy engaged the company to discuss how it would calculate the CO₂ emissions associated with the production of these chemicals. An issue of particular importance was how to estimate the amount of electricity used at its production facilities. The company was making positive efforts to visualize emissions, but it faced the challenge of selecting a cost-effective method with limited resources. We proposed a practical and straightforward estimation method that took into account Company C's current business scale and viability, while also referencing precedents from major companies. Our proposal helped the company move forward with a reasonable climate change response from the outset. The investment strategy will continue to monitor and engage with Company C.

<Column>

The Group is actively committed, through its operations, to activities that mitigate the negative aspects and enhance the positive aspects of our corporate impact on the environment. We have been particularly committed to helping realize the critical target of carbon neutrality by building and operating renewable energy power generation facilities using the framework of investment funds.

One example is the Group subsidiary SPARX Green Energy & Technology Co., Ltd. (SGET) conducting a pilot project to create a hydrogen supply chain for renewable energy in Tomakomai, Hokkaido*10. It was adopted as a model project by the Ministry of the Environment, and the renewable energy hydrogen plant began operations at the end of March 2025.

This pilot project aims to establish a system for stably producing and supplying up to one million Nm³ of green hydrogen derived from renewable energy sources annually by combining power generated from waste treatment facilities and solar power generation.*11 Hydrogen is a clean energy source that does not emit CO₂ and helps offset fluctuations in renewable energy output. However, cost is a significant challenge to its widespread use. Therefore, we aim to reduce costs and contribute to the local economy by powering the water electrolyzer with electricity supplied directly through our lines and surplus nighttime electricity from waste power plants. The hydrogen produced is transported via high-pressure trailers to local facilities and businesses for use in fuel cells and boilers. It helps reduce the kerosene consumption in this cold region.

The Group will bolster our response to global environmental issues through our investment management services and further disclose information on our efforts to address climate change issues.

- *10 SGET's concept of "Hokkaido as a Hydrogen Island" (adopted by the Ministry of the Environment for its "FY2023 Demonstration Project for a Low-Cost Hydrogen Supply Model Utilizing Existing Infrastructure")

- *11 Hydrogen production system utilizing waste and solar power generation at the Numanohata Clean Center in Tomakomai